Cryptocurrency mining is treated differently than buying, selling, or trading crypto. Any crypto received through mining is considered income. The IRS recognizes an income gain the day the cryptocurrency is successfully mined. This means that if you mine Litecoin (LTC) and receive 10 LTC on January 30, 2020, you would need to report this income on your 2021 tax return.

Mining cryptocurrency will create two taxable events. The first occurs when you successfully mine a crypto. You are then the owner of what the IRS considers property, or an intangible asset. The next taxable event occurs after you use, sell, or exchange the crypto.

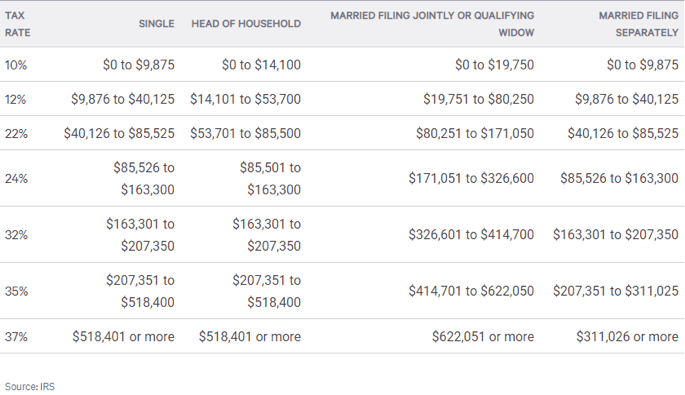

Using our previous example, if you mine 10 LTC at $45 each, you would earn $450 in income for 2020 that needs to be reported. The tax rate would equal your income tax rate, as found in the chart below.

If your income for the year was $50,000 filing as single, you would owe $99 ($450 x 22%).

As mentioned, you would have two taxable events for mining 10 LTC. The first is income for the year the coins are mined, and the second would be when the coins are sold, traded, or used. If the coins were sold, traded, or used in less than one year, you would pay short-term capital gains; if more than one year, you would by long-term capital gains. Refer to the question ‘How does the IRS tax bitcoin?’ for the specifics on how short- and long-term capital gains are taxed.

When mining, you’ll need to determine if you are a operating as a business or a hobby. This will adjust how your income from mining is filed. Finally, make sure to read up on how to assess the fair market value of the cryptocurrency interest you receive.